Bengaluru, NFAPost: Auto components industry to witness much sharper contraction in FY21 owing to pandemic aftermath and already weak automobile sales, states the Brickwork Ratings sector report on the Auto Components.

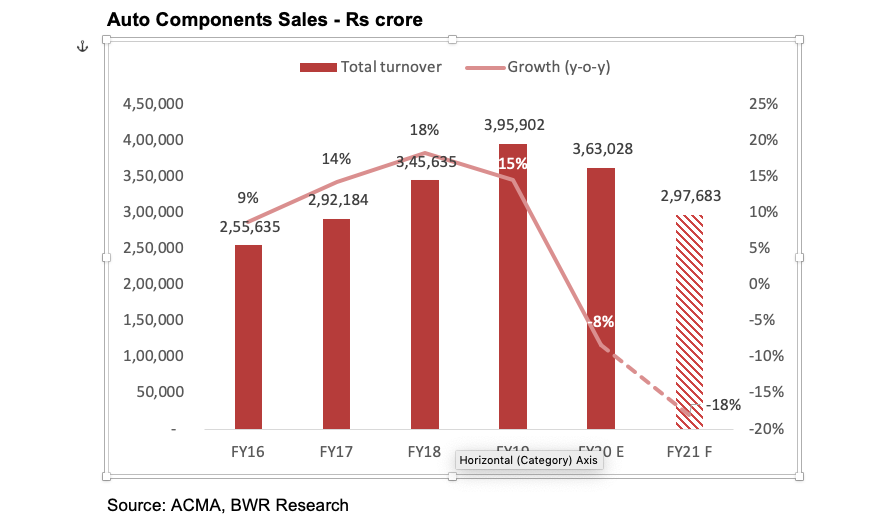

The report states, in FY20, auto components players’ revenues declined ~8-10% after a y-o-y increase until FY19 on account of a shrinking order book from Original Equipment Manufacturers (OEMs) due to lower automobile sales in the country during this period.

BWR expects the industry’s revenue to slip further and witness ~15%-18% decline in FY21 on account of lower income levels and continued weak sentiments.

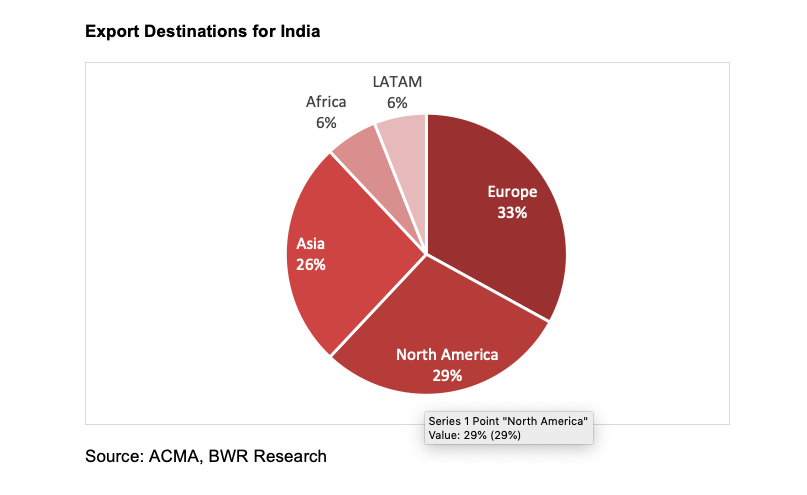

BWR expects export revenues to decline as well in FY21 as more than 50% of our exports are to markets in Europe, the UK and the US, and demand from these markets is expected to decline amid the COVID-19 outbreak and postponement of model launches or deferment/cancellation of orders.

Auto Components Sales – Rs crore

After a complete washout in April 2020 and minuscule sales in May 2020 due to the lockdown in the country, BWR expects auto components players will be affected adversely in Q1FY21, and to some extent, in Q2FY21.

However, a gradual recovery in sales is expected H2FY21 onwards due to pent-up demand, an improvement in OEMs’ production activities and the easy availability of credit from financial institutions; additionally, demand for two-wheelers and passenger vehicles is expected to rebound faster due to the preference for personal mobility over shared mobility or public transport on account of safety concerns in the pandemic situation. Furthermore, rural demand will continue to remain strong owing to a normal and well-distributed monsoon.

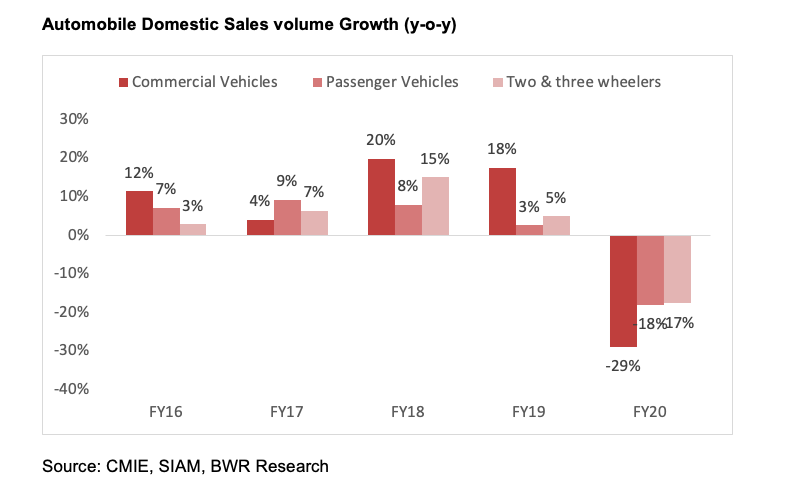

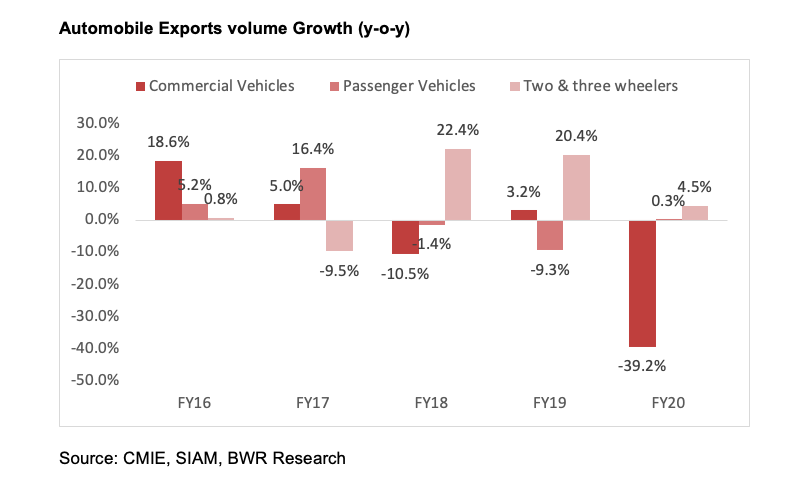

While domestic sales were already weak, exports also took a hit due to pandemic situation globally

Decline in the domestic sales of automobiles in FY20 has been the sharpest in the last eleven years on account of weak consumer sentiments arising from the slowdown in the economy, and exports have seen only a modest increase in FY20.

The sales of automobiles are expected to decline in FY21 due to the postponement of model launches, reduced production levels, supply chain disruptions and the slowdown in new capacity additions.

Automobile sales were weakest in the past decade. Almost all of the vehicle segments has seen a slump, commercial vehicles being the worst hit. Sales of CV in FY20 declined mainly due to excess load capacity (25%-30%) created in the market due to changes made to the axle load norms.

India exports around 27% of its automotive components production. US, Germany, UK, Italy, Turkey, UAE and Thailand are the largest export markets for auto components globally.

Over the past few years, India has emerged as the sourcing hub for many OEMs globally due to its cost-effectiveness in production and favourable geographical positioning to key markets such as the US, Europe and the Middle East.

However, due to Covid-19, exports have been impacted due to the cancellation or deferment of new orders, delay in shipments at ports and more than 50% of exports being to markets in Europe, the UK and the US, which have been the most impacted by the virus.

The domestic market has also been impacted due to the shutting-down of dealership and OEMs until mid- May 2020, labour shortage, the shortage in raw material availability, lower income levels and weaker consumer sentiments. Overall, Covid-19 has a negative impact on both domestic, as well as export markets.

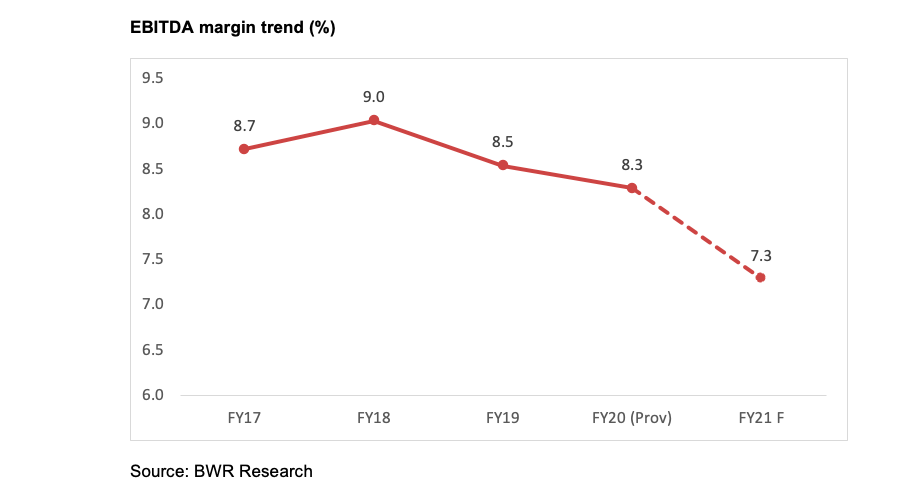

Profitability of auto component players to be hit owing to falling sales and implementation of stricter emission norms

The EBITDA margins have been declining since FY19 due to an increase in raw material costs and other promotional expenses. BWR expects to see, on average, a 100bps EBITDA margin decline in FY21 for auto components companies due to pricing pressure from OEMs as they may not be able to fully pass on price increases on account of the BS-VI norms in a subdued demand scenario.

The sector is likely to face challenges in the current fiscal due to the expectations of a continued weaker operating performance amid a challenging economic environment.

BWR has a neutral view for this sector in the medium term on account of pent-up demand, an improvement in OEMs’ production activities and the easy availability of credit from financial institutions.