It’s survival of the fittest as small to mid-sized developers stare at huge funding gap

Bengaluru, NFAPost: The already languishing residential real estate demand is expected to plunge 50-70% on-year in the current fiscal, with the Covid-19 pandemic crushing economic activity and with it, big-ticket spending.

As a result, the credit profiles of small-to-mid-sized and leveraged developers will be impacted than larger,

experienced developers with healthy balance sheets.

With demand going down, capital values will remain under pressure across cities. CRISIL expects a price correction of

5-15% across ticket sizes.

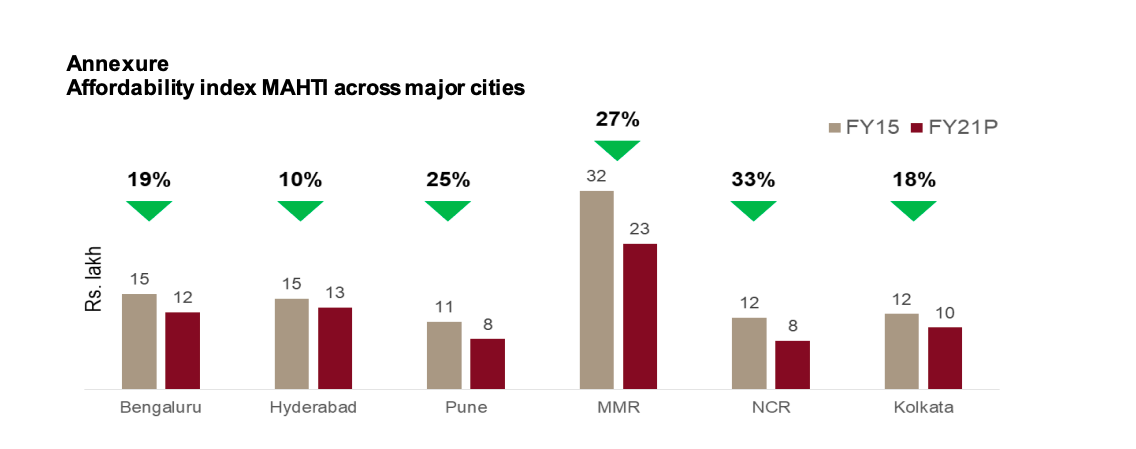

CRISIL Research Director Isha Chaudhary said lowering capital values and attractive interest rates augurs well for affordability which has improved by 10-30% across cities during the past five years- as measured by CRISIL’s proprietary index MAHTI1

“Despite improved affordability, demand translation will be feeble led by income uncertainty arising from pandemic coupled with weak investor sentiment emanating from pressure on capital appreciation / rental yields in the sector over past few years,” said CRISIL Research Director Isha Chaudhary.

While demand for new units will see a sharp decline, the blow to customer collections will be cushioned by advances against already sold inventory realised in line with construction progress.

RERA registration

The one-time relief for Real Estate Regulatory Authority (RERA)-registered projects2 would provide players an option to manage outflows through flexibility to delay construction spend. Postponing capex and land banking plans could be another way.

However, overall funding requirements are expected to rise as the hit in collections is expected to be far steeper than the decline in outflows due to deferred construction.

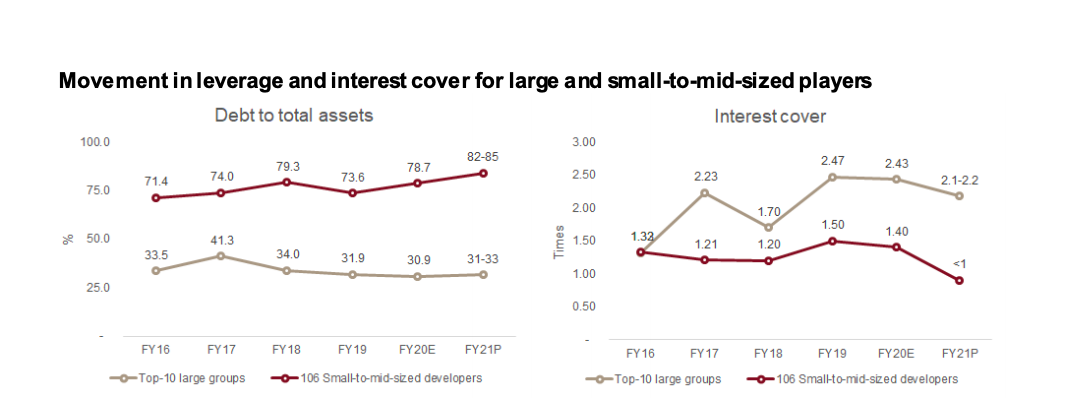

That said, large diversified players with strong delivery track record are expected to manage better as indicated by an analysis of the top 10 CRISIL-rated developer groups.

CRISIL Ratings Director Sushmita Majumdar said larger, established developers have ample financial flexibility, with debt-to-total assets ratio (a measure of leverage) estimated at a five-year low of ~30% as of end-fiscal 2020. Many will also have access to steady income from operational commercial assets.

“We estimate the increase in funding requirements for these players at only 15-25% higher than pre-pandemic

estimates,” said CRISIL Ratings Director Sushmita Majumdar.

The situation, however, is far bleaker for developers on the other side of the spectrum, as per CRISIL’s analysis of

more than 100 small developers and single-project special purpose vehicles.

Debt to total asset

Small-to-mid-sized developers will face a sharp ~200% rise in funding gap this fiscal. But their ability to borrow or raise capital is limited as debt-to-total assets ratio is significantly high at ~75% as of March 2020. Interest cover is also weak, at 1.2-1.5 times versus ~2.0 times for the large developer groups.

Given tight liquidity, some of these players will be vying for tie-ups with larger established names by way of joint-

ventures, joint development agreements, and development models to benefit from their processes and financial flexibility, or resort to distress sale of assets to raise funds.

Demand for the sector has been subdued over the past decade, on account of a raft of factors: demonetisation,

unaffordability, delay in completions etc. While income and employment generation remain monitorable, a mild recovery in residential demand might be expected in second half of the current fiscal, in the baseline case.

(The above story is based on CRISIL Research Report)