The start of 2021 has been on a positive note with Covid-19 vaccines approvals and distribution gaining momentum globally. The development of a new and more infectious Covid-19 strain in the UK and S. Africa, its spread to other nations, and renewed lockdowns challenge the efficacy, adequacy and timely availability of Covid19 vaccines. Nevertheless, the optimism around the visibility of vaccinations in the market remains intact, supporting risk-on sentiment.

Meanwhile, President-elect Joe Biden won both the seats in Georgia Senate run-off elections. This has increased the likelihood of further stimulus support in a Democrat-controlled US government. The Biden presidency is seen by markets as less politically volatile and more strategically stable in its foreign relations with key trade partners. It remains to be seen whether Biden will de-escalate trade tensions with China post the inauguration ceremony on 20th January.

Notably, the EU and UK struck a last minute ‘soft’ Brexit deal end-December, after four years of unsettling negotiations. With this, the UK has made a formal exit from the bloc. The agreement places no tariffs or quotas on goods trade between the bloc and UK post 31st December however custom duties and border checks will be applicable. The biggest setback in the deal is faced by the services sector, in particular, the UK financial markets, which loses its easy access to the EU financial markets. This is likely to weigh down on UK’s economic recovery at a time of rising COVID-19 cases, new COVID-19 variant and third national lockdown.

On the domestic front, the government released its first advance estimate of FY21 national income where it pegged India’s FY21 real GDP and GVA growth at -7.7% and -7.2% respectively. This is the first time India would see this sharp contraction since 1950’s. From a sectoral lens, agriculture is the only sector in FY21 that maintained a strong growth momentum of 3.4% in both H1 and H2 FY21 due to healthy kharif output, better prospectus of rabi sowing, and policy reforms supporting the rural economy.

While the RBI has already stepped in to offset the impact of GDP contraction on social, financial and macroeconomic variables, in our view, we are nearing an end to further monetary policy easing. There has been a growing expectation in the market that RBI would soon deploy measures to soak up excess liquidity. Basis the anticipated durability in growth conditions we believe that the RBI would start absorbing excess systemic liquidity sooner-than-later. The focus on supporting economic growth now shifts onto the fiscal reforms for which Budget FY22, scheduled for release on 1st February, holds significance (for details, referFY21 GDP growth estimated at a historical low, dated 7 January, 2020).

Manufacturing & Services PMI index: A mixed bag

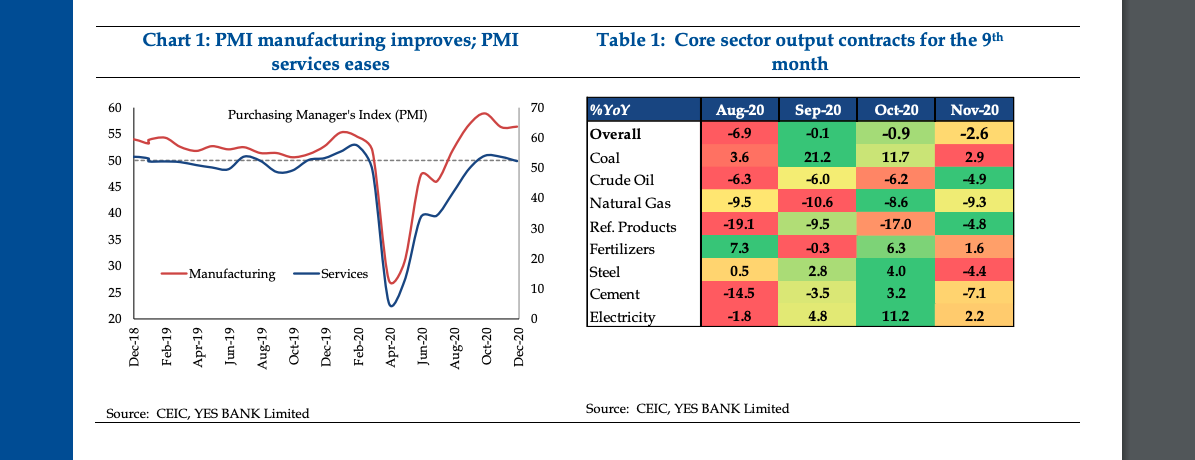

India’s Manufacturing PMI index remained almost steady at 56.4 in Dec-20 vis-à-vis 56.3 in Nov-20. With this print the manufacturing sector expanded for the fifth consecutive month. Relaxation of COVID-19 restrictions and strengthening of domestic demand supported the recovery of manufacturing sector with factory orders and input buying firming up. The stock of finished goods continued to decline during the month due to strong sales growth. Exports orders expanded as well however, the pace of expansion was the slowest in four months due to renewed global lockdowns. Employment and inflation remained pain points within the manufacturing sector with employment levels declining further during the month and input cost inflation rising to a 26-month high. Overall, firms remained cautiously optimistic about increase in output levels over one-year horizon.

Services PMI index came in at 52.3 in Dec-20, falling from 53.7 in Nov-20. The increase in domestic output was the slowest in the 3-months to Dec-20 as the increase in COVID-19 infections affected services demand. Globally, the demand for services decreased sharply due to increase in global infections rate, renewed restrictions and travel ban. Employment levels continued to decline however, the decrease was marginal during the month.

Input costs increased for the firms due to higher prices of fuel and other raw materials. Some sectors introduced discounts to stimulate demand amidst higher firm level competition. Looking at the services sector from a sectoral lens, transport & storage, finance & insurance, and consumer services expanded during the month while information & communication and real estate & business services contracted. Though firms remained optimistic for 2021, however the level of optimism fell from Nov-20.

The composite PMI index fell to 54.9 in Dec-20 from 56.3 in Nov-20 due to slower rate of expansion in both services and manufacturing sector output. While domestic demand has shown improvement since the phased unlock, the pace of improvement has begun to moderate. Increase in COVID-19 cases in India and abroad affect the domestic output and export orders respectively. Overall, business conditions are expected to improve with vaccines rollout in process but the pace of ongoing improvement may falter in case of any delays.

Core sector growth dips further While trend in core sector growth improved after contracting by 37.9% in Apr-20, it continues to trail in negative territory for nine consecutive months now. For Nov-20 core sector growth dipped by 2.6% YoY from -0.9% in Oct20. The dip is likely to be on account of post-festive season moderation in overall output. After a brief respite, steel and cement production contracted on an annual basis in Nov-20.

However, we expect that Government’s focus on infrastructure sector and demand visibility from real estate segment to be supportive of overall steel and cement production. However, shortage of iron ore primarily led by closure of major mines in India is expected to cause near term disruptions in steel production. Within the energy space, barring coal, production in all other subsectors including crude oil, natural gas and refinery production continued to decline due to operational issues, closure of wells and lower demand.

Electricity output continued to expand for the third consecutive month led by increase in production of thermal electricity.

Fertilizer production also recorded an expansion led by demand impetus amidst Rabi sowing. For H2 FY21, with pickup in demand, government’s supportive policy and some impact from favorable statistical base we expect core sector growth to normalize. Recent impetus to production in the form of Production-Linked Incentive Scheme to more than 10 sectors is also expected to augur well for overall output.

Central Government’s fiscal position remains worrisome

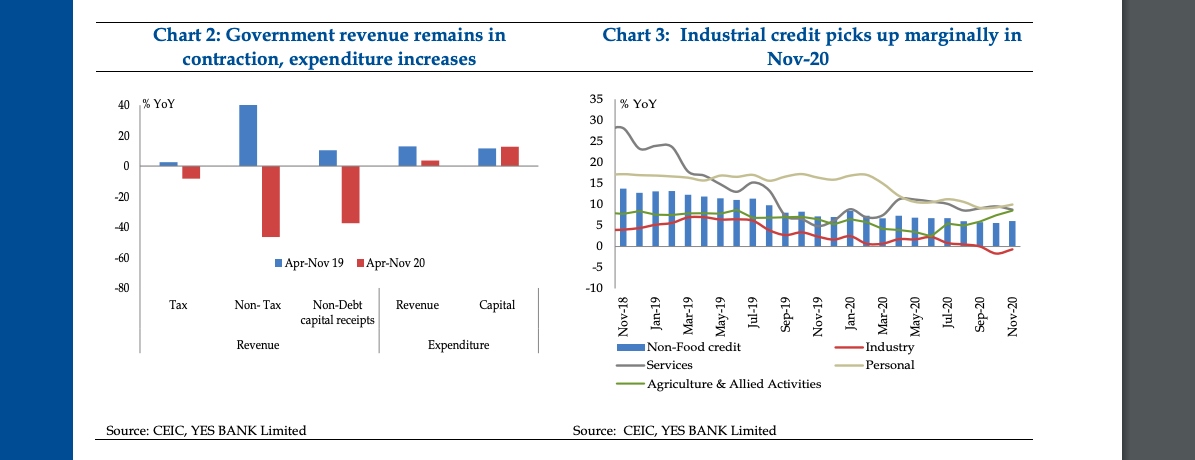

Fiscal Deficit for FYTD 21 (Apr-Nov 20) rose to 135% of the full year target as compared to 105.4% a year ago. While gross tax revenue in FYTD 21 contracted by 12.6% YoY vs. +0.81% over the same period last year, on an annual basis it grew by double digits in Nov-20 led by a strong increase in indirect tax collections.

Looking at the overall monthly trend, direct tax collections have been improving with Nov-20 recording a growth of 14.0% YoY from 7.4% YoY in Oct-20. Gradual improvement in income tax collection is encouraging and in line with pick up seen in leading demand indicators.

Indirect tax collections recorded an expansion of 27% YoY in Nov-20 from 23.6% YoY in Oct-20 led by a broad based increase in Excise duty, Custom duty and GST revenue. Talking about FY21, so far, excise duty collection is the only component to have recorded growth for six consecutive months now. This can be attributed to the steep hike in taxes on petrol and diesel. Custom duty also recorded an expansion after seven consecutive months of contraction. At INR 1.15 tn, GST collections pertaining to the month of Nov-20, jumped to a record high. This has been the third consecutive month where collections have remained above the INR 1 tn mark. The increase in GST collections was likely on account of better compliance, festive tailwinds and pent-up demand amidst unlocking of economy.

Total expenditure for FYTD 21 stands lower at 4.7% as compared to 12.8% in corresponding period of FY20. Encouragingly, capital expenditure shot up significantly by 248.5% YoY in Nov-21, thereby taking overall capex in FYTD 21 to 12.8% higher than 11.7% YoY recorded in corresponding period of FY20. Revenue expenditure also increased marginally with sectors like agriculture, rural development, health and family welfare recording a healthy expansion.

While the recent high frequency indicators have underscored expectations of faster than expected normalization, we remain cautious as the possibility of loss in the growth momentum persists with conclusion of festive season. Despite recent traction in GST collections, increase in customs and excise duties collections, we expect government finances to remain strained and continue to view fiscal deficit at 7.5% in FY21 (BE: 3.5%).

Credit growth records an uptick led by festive tailwinds

Total credit offtake by Scheduled Commercial Banks posted an uptick of 6.0% in Nov-20 from a 3-year low growth of 5.5% YoY in Oct-20. Basis granular data released by RBI, improvement was led by growth in Agriculture sector followed by Personal loans segment. On the other hand, growth for Services sector moderated while Industrial credit growth contracted for the second consecutive month.

Agricultural credit growth increased significantly to a 17 month high of 8.5% YoY from 7.4% in the previous month. The expansion is on the back of a healthy kharif output and better prospects of rabi sowing, along with a gradually trickling down of supportive measures announced by the government.

Credit growth extended towards Personal loans ticked up by 10.0% YoY in Nov-20 from 9.3% in Oct-20. Demand in personal loan segment has recovered likely on account of banks charging lower interest and processing fee during festive season. On sub-sector basis, credit growth for vehicles, consumer durables followed by credit cards recorded an increase.

Credit growth to Services sector fell marginally coming in at 8.8% YoY in Nov-20 from 9.5% in Oct-20. At a granular level, credit offtake to professional service segment declined significantly. However, credit growth for tourism & hotels and transport operators recorded an improvement.

Industrial credit contracted by 0.7% YoY from -1.7% YoY in Oct-20. It is important to note that post the launch of Emergency Credit Line Guarantee Scheme (ECLGS) credit growth for small and medium enterprises have improved significantly. As per the latest data available, so far banks have sanctioned INR 2.05 tn to about 81 lakh accounts of the sanctioned INR 3 tn under ECLGS. However, credit growth for large enterprises continued to contract for the third consecutive month. On sub-sector basis, major drag came from infrastructure, cement, engineering and textiles sector.

The pace of credit growth has continued to wither so far in FY21 despite collaborative efforts by the RBI and the Government. Going forward, a marginal uptick in credit growth can be expected with banks witnessing some traction in demand due to improving overall economic scenario. Nevertheless, overall credit growth is expected to remain muted at ~5-6% in FY21 as most banks have strengthened their risk and underwriting mechanism and have been concentrating on maintaining their asset quality.